From Hosting Innovation to Owning It: Why UK Life Sciences Policy Must Shift Focus from Multinationals to Scaling Domestic Biotech

Executive summary

The UK Government has placed Life Sciences at the centre of its industrial strategy, committing substantial public funding and positioning the NHS as a global platform for research, innovation and investment. The Life Sciences Sector Plan sets out clear ambitions: to attract international investment, accelerate clinical research, and support UK-based companies to scale, remain anchored in the UK, and become global leaders.

These ambitions sit squarely within the Government’s wider Growth Mission, which seeks to translate public investment in science into productivity, high-value jobs and long-term economic return for the UK. The Life Sciences sector is intended to be both a scientific strength and a driver of sustainable economic growth.

This paper argues that, despite this stated ambition, current policy design and funding allocation are failing to deliver these objectives in a sustained way. The UK remains a global leader in discovery science and early research, but continues to underperform in commercial clinical trials, struggles to retain and scale UK-headquartered Life Sciences companies, and systematically exports high-value intellectual property and long-term economic returns overseas.

Moreover, we argue that achieving Government’s expressed ambition could distract us from ongoing failure. The Government states that by 2030 the UK will be the leading Life Sciences economy in Europe; and by 2035, the third most important Life Sciences economy globally, behind only the US and China. But as these economies accelerate away, an increasingly distant third place will be little consolation if it comes without substantial economic growth.

The core problem is not a lack of intent or headline investment, but the structure of public support. UK Life Sciences policy is over-optimised for upstream discovery and for servicing large multinational pharmaceutical companies, while providing limited, fragmented and unreliable support for domestic companies at the point of greatest vulnerability: the transition from pre-clinical development into early clinical trials. This is the stage at which capital requirements rise sharply, execution risk is highest, and delays or uncertainty can force premature sale or relocation. In a system that treats all sponsors equally, multinational companies can operate flexibly across jurisdictions, while UK SMEs bear disproportionate risk.

Recent public funding settlements reinforce this imbalance. Although UK Research and Innovation has received a record multi-year budget allocation, the overwhelming majority of funding continues to flow towards academic research, research infrastructure and enabling systems. Only a small fraction is explicitly directed at supporting UK-headquartered Life Sciences companies through early clinical development, despite this being a stated priority of the Life Sciences Sector Plan. As a result, public investment frequently de-risks innovation for others, while ownership, scale-up and long-term value creation accrue elsewhere.

The consequences are visible across the ecosystem. Commercial clinical trial recruitment continues to decline, early clinical execution remains slow and unpredictable, and UK-originated assets are routinely transferred into overseas-headquartered companies before clinical value inflection. While partnerships with multinational firms deliver short-term activity and investment, they also reflect a deeper shift: the UK increasingly competes to host innovation rather than to own it.

Neutrality in policy design (by which we mean a system that treats all sponsors equivalently regardless of size, ownership or strategic importance), and the assumption that identical rules produce fair outcomes, is no longer sufficient. If the UK intends to build globally competitive Life Sciences companies, it must make a deliberate choice to support domestic companies at the point where failure or premature exit is most likely. That requires moving beyond discovery-first funding and undifferentiated delivery towards targeted, time-bound and transparent interventions that align public investment with domestic ownership, scale-up and long-term economic return.

Without such a shift, the UK risks entrenching a model in which it discovers, de-risks and exports Life Sciences value, becoming a world-class service economy for global innovators rather than a world-class owner of Life Sciences innovation.

The clinical trials paradox: activity without competitiveness

The NHS is often described as one of the UK’s greatest strategic assets for Life Sciences. Yet current data reveal a profound imbalance in how this asset is used.

In 2024/25, over one million participants took part in studies supported by the NIHR Research Delivery Network. Fewer than 40,000 of those (approximately 4%) were recruited into commercial clinical trials, despite those trials delivering disproportionately high value to the NHS, estimated at over £30,000 per participant, equating to more than £1.2 billion in total benefit.

This points to a system that is highly active in research overall, but weak in the very category of research government is most keen to attract and grow: globally competitive commercial studies.

The O’Shaughnessy Review correctly identified this challenge and set out ambitious goals, including doubling commercial trial recruitment, accelerating trial delivery, and positioning the NHS as a global platform for health R&D. Since publication, and despite substantial targeted investment and regulatory reform, these ambitions have not been realised.

According to the most recent ABPI data:

While the number of interventional industry trials has recovered from its immediate post-COVID collapse, this recovery merely returns the UK to the level predicted by a long-term downward trajectory since 2015.

Recruitment into commercial trials has fallen year-on-year and is now at its lowest level since 2017, despite a 35.7% increase in the number of interventional trials initiated in 2024 compared with 2023.

Early indications for 2025 are not encouraging. MHRA data show overall trial application growth of just 9% year-on-year, with the strongest growth in early-phase studies where recruitment demands are typically lower. This suggests that while the UK may be becoming better at starting trials, it remains weak at delivering them at scale, particularly in globally competitive, time-sensitive studies.

It is central to our argument that NHS research infrastructure requires sustained investment and, in some areas, structural reform. Capacity constraints, workforce pressures and operational variability affect academic and commercial sponsors alike. Without reform, the NHS risks functioning as a binding constraint on the entire UK research ecosystem, rather than as the strategic differentiator it is often described to be.

However, the purpose of reform matters as much as its content. Reform should be understood not as a cost to be managed, but as an investment in the Government’s Growth Mission and designed explicitly to support the scaling of domestic UK Life Sciences companies. Crucially, the impact of current system frictions is not evenly distributed. Large multinational pharmaceutical companies can absorb delays, re-sequence programmes across jurisdictions, and rely on established global trial networks; the ABPI’s own clinical trials data suggest they continue to do so. UK SMEs cannot. For smaller companies, slow site set-up, uncertain timelines or modest cost increases can be existential.

A system that is formally “neutral” therefore operates asymmetrically in practice, systematically disadvantaging domestic innovators. Reform designed primarily to improve the UK’s attractiveness to global sponsors risks entrenching this imbalance. By contrast, reform designed around the needs of capital-constrained, UK-headquartered companies, predictable timelines, reliable delivery and early clinical momentum, would raise performance for the system as a whole. If the NHS can deliver consistently for domestic SMEs, it will, by definition, be competitive for global pharmaceutical companies as well. The reverse may not be so true.

Ambition without differentiation: neutrality as structural bias

The Life Sciences Sector Plan repeatedly emphasises the importance of UK SMEs and the need to support domestic companies to scale. However, the delivery framework underpinning this ambition remains largely size-blind and sponsor-neutral.

Of the four headline metrics used to assess success:

Three focus on aggregate R&D investment, patient access and foreign direct investment.

Only one partially reflects UK company growth, and even that permits overseas ownership, IP migration and offshoring of value.

The result is a strategy optimised for activity in the UK rather than ownership and control by UK companies. High-profile partnerships with multinational firms are presented as unambiguous successes. These collaborations undoubtedly bring near-term investment, jobs and trials, but they also illustrate a deeper pattern: the UK increasingly competes to host innovation rather than to retain it.

Neutrality in this context is not benign. Large pharmaceutical companies can navigate system friction, while UK SMEs face concentrated risk. Treating all sponsors equally therefore entrenches existing asymmetries and reinforces incentives for early sale or relocation.

A discovery-first system by design

These outcomes are not accidental. Recent public funding settlements make clear that the UK Life Sciences ecosystem is explicitly structured around academic excellence, institutional stability and research infrastructure, with company scale-up treated as a downstream consequence rather than a core objective.

The question is not whether the UK should continue to invest in discovery science; it must. But rather whether a discovery-led funding model alone can deliver the Government’s stated objectives on economic growth, global competitiveness and long-term domestic ownership. In practice, the majority of public funding is directed towards curiosity-driven research, research institutes and enabling infrastructure. The UK Research and Innovation (UKRI) four-year funding agreement illustrates this clearly. While these investments are essential and valuable, they overwhelmingly reward inputs, grants, publications, facilities and trial starts, rather than outcomes such as companies carried through clinical inflection points, assets retained through phase II, or UK-headquartered balance sheets capable of independent growth.

This bias is well documented. A recent CPI report commissioned by the Office for Life Sciences highlights a persistent scarcity of translational funding to bridge the gap between academic research and commercial readiness. Interviewees consistently described a funding landscape that supports discovery on one side and late-stage ventures on the other while leaving early commercialisation structurally under-supported. As one founder put it:

“Getting from that purely research grant to data you can put in front of investors is the main problem for everyone.”

This “valley of death”, requiring proof-of-concept data, regulatory planning and early business development, is rarely funded by either traditional research grants or private seed capital. Accelerators can play a valuable role, but their scale remains limited relative to national need. As one investor noted bluntly:

“No corporate entity or investor is going to play in that area. So we think the answer has to be government.”

Translation is therefore framed rhetorically as a bridge between academia and industry, but in practice treated as an endpoint. Spin-out formation, licensing and early proof-of-concept are implicitly assumed to represent success. What follows, capital intensity, regulatory execution and sustained clinical development, is left to global markets.

In Life Sciences, this assumption does not hold. Early clinical development is precisely the stage at which private capital is most risk-averse, timelines are longest and execution risk is highest. The CPI report further identifies a second structural cliff edge after initial commercialisation, as companies struggle to secure follow-on capital, navigate regulation and achieve NHS adoption.

The system therefore behaves exactly as designed. Universities are incentivised to out-license early. Technology transfer offices are incentivised to maximise deal flow rather than long-term value retention. Founders are incentivised to exit when overseas capital offers greater certainty of progression. Investors are drawn to jurisdictions with faster clinical execution and more reliable access to scale capital.

It is a layered failure. The policy architecture is discovery-first, translation-light and scale-up blind. The loss of domestic ownership is not a failure of ambition or capability, but a predictable consequence of policy design.

Metsera: a case study in premature value leakage

The consequences of this approach are not abstract. They are illustrated clearly by the recent trajectory of Metsera.

Metsera’s pipeline includes assets originating from UK academic research. In particular, Zihipp, a UK spin-out based on research from Imperial College London and supported by IP Group, developed obesity and metabolic drug candidates that later became part of Metsera’s portfolio. In 2023, Zihipp was acquired by Metsera. While UK stakeholders retained rights to upfront, deferred, milestone and royalty payments, they did not retain exposure to downstream value creation.

Metsera itself was founded in the United States and went on to raise approximately $290 million in venture capital, enabling rapid progression into and through clinical development. In January 2025, Metsera completed an IPO at a valuation of approximately $1.8 billion. Later that year, it was acquired by Pfizer for $4.9 billion upfront, with total potential value reportedly reaching approximately $10 billion subject to milestones.

Incidentally, not a single UK biotech completed an IPO in 2025, marking the third consecutive year with no new listings.

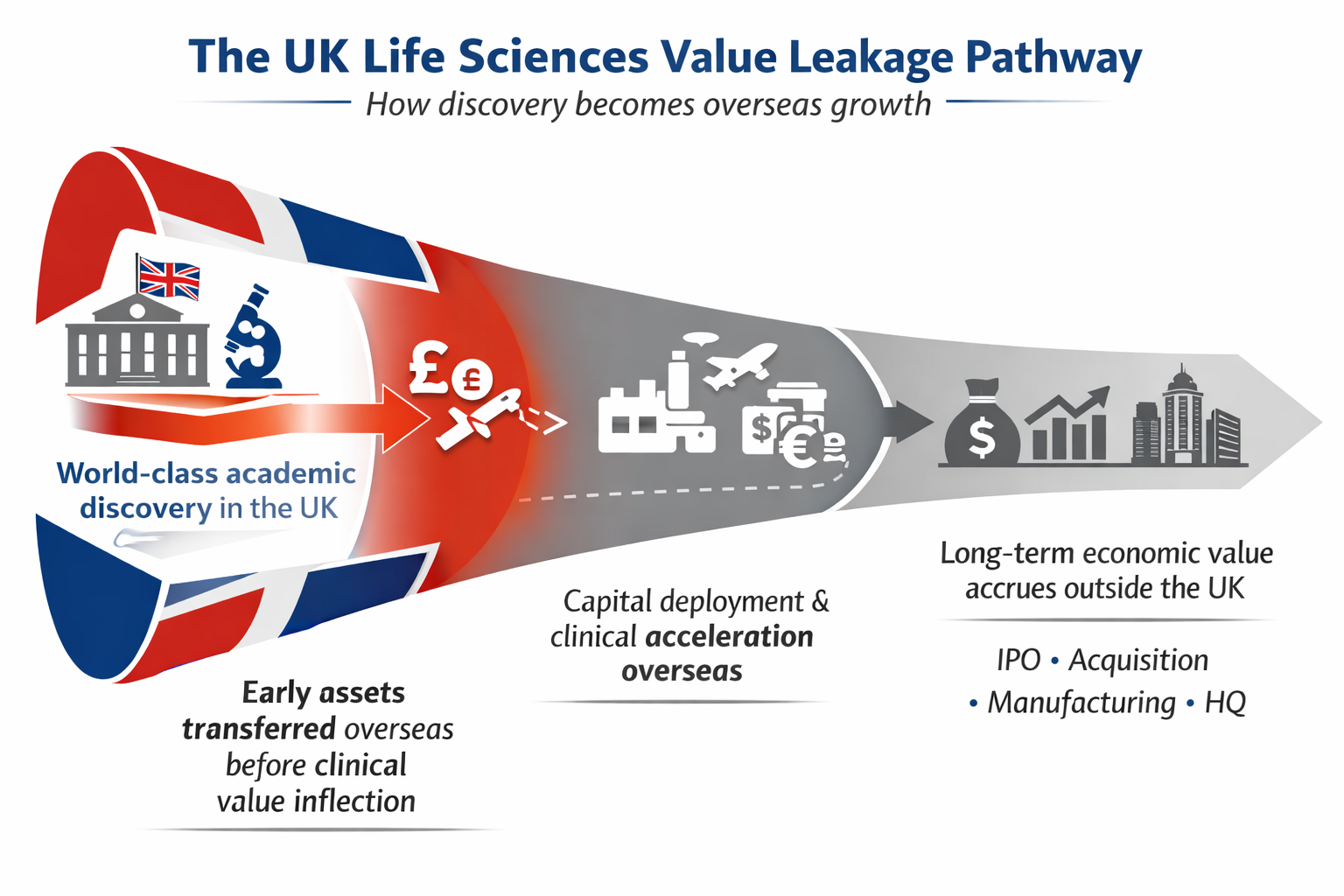

Each step in this journey reflects rational decisions by individual actors. Taken together, they illustrate a recurring pattern:

world-class academic discovery occurs in the UK;

early assets are transferred overseas before clinical value inflection;

large-scale capital deployment and clinical acceleration occur elsewhere;

and the majority of long-term economic value accrues outside the UK.

This is not a failure of science or entrepreneurship. It reflects a system in which UK-originated innovation lacks access to sufficiently rapid, well-capitalised domestic pathways into early clinical development. Where those pathways do not exist, selling early becomes the rational choice.

From systemic diagnosis to targeted intervention

The Life Sciences Sector Plan includes a commitment to establish a dedicated service to support 10–20 high-potential UK Life Sciences companies to scale and remain anchored in the UK. This acknowledges that neutrality alone has not corrected the scale-up gap.

For this commitment to succeed, support must be concentrated at the point of greatest vulnerability: the transition from pre-clinical development into early clinical trials. Without intervention at this stage, downstream initiatives arrive too late to influence company trajectory.

There is also a tension between this commitment and the wider funding settlement, which continues to prioritise academic and system-level investment over company balance sheets. Without explicit capital reallocation or ring-fenced mechanisms focused on early clinical execution, the commitment risks functioning as a signal of intent rather than a determinant of behaviour.

Operationalising this approach would require:

explicit and transparent eligibility criteria;

time-bound, milestone-linked support;

aligned public co-investment, prioritised trial access and early regulatory engagement.

This does not constitute “picking winners”, but a proportionate response to a known market failure.

Why now? A narrowing window for competitiveness

The case for a more deliberate approach to supporting UK Life Sciences scale-up is not only structural, but timely. Several external shifts mean that the costs of inaction are rising and the opportunity for corrective intervention is narrowing.

First, the international bar for competitiveness is moving. Comparator jurisdictions are no longer relying solely on scientific excellence, tax incentives or late-stage inward investment, but are actively re-engineering clinical, regulatory and funding systems to retain domestic innovators through early development. The European Union’s proposed Biotech Act, for example, goes beyond coordination and rhetoric. It includes explicit proposals to accelerate clinical trial approvals, make it easier to manage multi-country clinical trials in the EU, create regulatory sandboxes for novel modalities, reduce administrative burden for SMEs, and improve access to scale-up capital for European-headquartered companies.

In the United States, the approach is different but no less deliberate. For example, ARPA-H funding uses milestone-based, execution-focused models that prioritise speed, delivery and scale rather than discovery alone. Combined with faster clinical execution, deep capital pools and regulatory familiarity, this creates an ecosystem that pulls promising companies through early development rather than pushing them towards early exit. The common feature across these jurisdictions is not protectionism, but intent: public systems are being reshaped to reduce uncertainty and compress timelines at the company level.

Finally China. A country whose activity is growing so quickly that it cannot be ignored in this debate. Early clinical development has been treated explicitly as a strategic capability rather than an administrative function. Over the past decade, China has restructured its clinical trials ecosystem through nationally coordinated hospital networks, accelerated ethics and regulatory review timelines, acceptance of overseas clinical data, and active alignment between regulators, public hospitals and state-backed capital. For domestic biotechs, this translates into faster progression from pre-clinical work into first-in-human and proof-of-concept studies. These reforms were not designed to favour individual firms, but to retain national value by ensuring that promising Chinese-origin assets reach clinical inflection before global competition intervenes.

By contrast, while the MHRA is showing renewed vigour under new leadership, the UK has yet to fully exploit the regulatory flexibility created by Brexit. The COVID pandemic briefly demonstrated that faster approvals, parallel review, pragmatic risk tolerance and system-wide coordination were possible when treated as priorities. However, these emergency adaptations were not systematically translated into business-as-usual regulatory and delivery models. Instead of consolidating those gains, the system largely reverted to pre-existing processes, incrementally improved but structurally unchanged. This represents a missed opportunity to convert crisis-driven innovation into a durable competitive advantage.

Second, global uncertainty is reshaping investment behaviour. Volatility in US policy, capital markets and trade relations is already influencing how and where Life Sciences capital is deployed. While this creates risks, it also creates opportunity. Countries that can offer credible, predictable and well-capitalised pathways through early clinical development stand to capture companies that might otherwise default to US-led scale-up. Without such pathways, the UK will remain exposed to capital flight precisely when strategic realignment could work in its favour.

Third, recent UK funding settlements have created a moment of policy clarity. The scale and structure of UKRI’s multi-year allocation make explicit the government’s current priorities. If these allocations are allowed to embed without adjustment, they will lock in a discovery-first, scale-up-light model for the remainder of the Spending Review period. Conversely, modest but targeted rebalancing now could have outsized impact by shaping behaviour, expectations and investment decisions at the point where companies are most sensitive to policy signals.

Finally, the pipeline of UK-originated assets approaching early clinical inflection is substantial. Advances in genomics, AI-enabled drug discovery, cell and gene therapies and novel trial designs mean that the coming years will see a growing number of UK-founded companies facing the same structural cliff edge identified in this paper. Without intervention, the pattern of premature exit and overseas relocation will accelerate, not diminish.

Taken together, these factors mean that the question is no longer whether the UK should address the scale-up gap, but whether it does so while it still has leverage. The fight to be the third most important Life Sciences economy globally by 2035 is growing increasingly competitive, at the same time third place is looking increasingly distant from the battle between US and China for supremacy.

Delay will not preserve optionality. It will simply allow existing incentives to continue shaping outcomes.

Conclusion: from neutrality to intent

The UK has built a world-class Life Sciences discovery ecosystem and a globally attractive research platform. What it lacks is a deliberate strategy to convert those strengths into sustained domestic ownership and scale.

Recent funding settlements make this choice explicit. The UK continues to prioritise academic excellence, institutional stability and research infrastructure while allocating limited capital to the risky, time-sensitive process of scaling domestic Life Sciences companies. This is not a failure of execution, but a reflection of what the system is designed to reward.

Countries that lead in Life Sciences do not treat company scale-up as an accidental by-product of discovery. They fund it deliberately, at scale and at the point of maximum vulnerability.

The question is no longer whether the UK can attract Life Sciences innovation. It is whether it intends to keep what it creates.

That’s the diagnosis. What is the prescription?

At the outset, we made it clear that this paper should be read in the context of the Government’s growth mission and its stated ambition to translate public investment in science into productivity, high-value jobs and long-term economic return for the UK. The analysis above suggests that, while the UK’s discovery engine is strong, current policy and funding structures are not yet aligned with that growth objective at the point where scale-up is decided.

This moment also coincides with significant institutional change. UKRI is actively reshaping its funding architecture, with a new strategy expected shortly. While this process has created uncertainty across the system, it also represents a rare window to address long-standing structural gaps, particularly around early clinical development and scale-up.

If the UK genuinely intends to retain and scale domestic Life Sciences companies, incremental reform will not be sufficient. The challenges described in this paper are structural, and addressing them requires an equally structural shift in how public policy, funding and system assets are deployed. If growth is the objective, scale-up is the mechanism.

The UK must ensure coherence, clarity and navigability to its life sciences support landscape.

At present, the system is fragmented across multiple agencies, programmes and funding streams, each individually rational but collectively complex. Innovate UK, NIHR, UKRI councils, the Office for Life Sciences, regional initiatives, and charity and university programmes all provide valuable support. However, from the perspective of scaling companies, this landscape often appears opaque, duplicative and difficult to navigate, particularly at the precise moment when execution speed is critical and management bandwidth is constrained.

This fragmentation carries real economic consequences. Companies with limited runway must spend disproportionate time navigating funding processes rather than executing clinical and operational milestones. Opportunities are missed not because support does not exist, but because it is difficult to access in a timely, predictable and strategically aligned way.

The UK requires a more integrated operating model, in which scale-up support through a coherent national pathway aligned explicitly with the objective of building globally competitive, UK-headquartered companies. For example, this could include a single national ‘front door’ and concierge function for scaling Life Sciences companies, mapping and brokering support across UKRI, NIHR, OLS. This should include interfacing with the regional and devolved complexity across health systems and regional growth bodies. The integrated operating model would need to cover governance, the process and monitoring of the success of the model. Of note, this would need to focus on navigation and alignment that is relevant for the individual company, not a one-size fits all.

Encouragingly, Innovate UK is already developing new approaches to identifying high-potential companies and providing more coordinated, concierge-style support. This is an important and welcome development. As this work progresses, it will be essential that eligibility criteria, delivery mechanisms and governance arrangements are shaped with meaningful input from industry, investors and system practitioners, including organisations such as the BioIndustry Association, to ensure that support reflects the operational realities of scaling companies.

2. Government must establish clear, national criteria for identifying and supporting UK Life Sciences companies at critical scale-up inflection points.

The Life Sciences Sector Plan specifically calls for targeted scale-up support for 10-20 companies each year. If this is going to happen, the Government must get on and create the criteria and the mechanisms for deploying that support urgently.

Eligibility criteria should be transparent, time-limited and grounded in objective indicators of strategic importance. These may include UK-anchored intellectual property, proximity to clinical value inflection, credible pathways to independent scale, and the potential to generate substantial long-term economic and health benefits, such as platform technologies with significant future potential or contribution to priority disease areas.

Such criteria should not be used to permanently designate winners, but to identify companies for time-limited, execution-focused support at the precise stages where market failures are most acute. The process for defining and applying these criteria should involve experienced industry leaders, investors, research charities, academia and regional representatives ensuring that selection reflects execution reality. Selection decisions, and the performance of selected cohorts, should be transparently reported and independently evaluated.

We understand Innovate UK is already working on such criteria; we would strongly encourage early engagement with the community and with proven life science commercial leaders.

3. Public funding must have increased emphasis towards early clinical execution.

This does not imply reducing support for discovery science, which remains essential. However, it does require acknowledging that the transition from pre-clinical development into phase I and early phase II trials represents the point of greatest strategic vulnerability for UK-headquartered companies.

Support at this stage should be delivered through targeted, proportionate and legally compliant mechanisms, such as co-funding grants covering a defined proportion of eligible clinical trial costs, subject to clear ceilings, co-investment requirements and demonstration of public benefit (e.g. inclusion of underserved populations, or locating trials in areas of unmet need). The UK’s Subsidy Control Act and international obligations already provide structured routes for such support, particularly where it addresses clear R&D market failures and generates broader economic and societal spillovers.

Well-designed schemes, that interface well with existing schemes, could materially reduce the effective cost of early clinical development for UK-based activity, without requiring unlimited subsidies or discriminatory protections. Crucially, support should be tied to clearly defined objectives, including clinical advancement, domestic capability building and knowledge generation.

Equally important is flexibility. Funding mechanisms must be accessible to companies with limited financial runway and should operate at timelines consistent with commercial execution, rather than academic grant cycles. Capital deployed too slowly fails to achieve its strategic purpose.

4. Regulatory access, data, clinical infrastructure and system interfaces should be deployed deliberately as strategic national assets.

The UK’s integrated healthcare system, regulatory expertise and clinical research infrastructure represent globally distinctive strengths. However, these assets are not currently configured to provide execution certainty for scaling domestic companies.

A UK clinical development “passport”, that integrates new and existing initiatives, could provide qualifying companies with coordinated regulatory and clinical system access (including potential access to data assets, subject to robust governance), prioritised scientific advice, streamlined approvals, and a single accountable interface spanning MHRA engagement, research approvals and NHS trial delivery. This passport would be distinct from existing initiatives offered to individual medicines; it would operate at a company level, eligibility determined by a minimum level of investment in the UK, including being UK domiciled. A further initiative could be developed to offer systematic support for patient and public involvement.

Importantly, this need not rely on unlimited or unlawful subsidies. Regulatory and clinical support could be structured as targeted R&D support, delivered proportionately and transparently, and tied to clearly defined public policy objectives such as strengthening national clinical research capability and improving patient access to innovation. It is important to note that prioritisation of domestic scale-ups must not exclude non-UK companies or academic trials but should be handled via transparent criteria and capacity planning.

Such support should be framed not as preferential treatment, but as deliberate deployment of national infrastructure to achieve stated economic and health objectives.

And while such actions may currently be challenging under the UK’s subsidy control framework, it could be enabled through narrowly targeted R&D “streamlined routes”, by structuring NHS‑run trials as open research infrastructure available on objective criteria, or by amending the regime to create a specific, health‑focused innovation exemption that still meets the UK’s international subsidy commitments.

5. The NHS must be actively enabled and incentivised to function as a globally competitive clinical development partner.

Research delivery constraints within the NHS affect all sponsors, but they disproportionately disadvantage smaller domestic companies, which lack the financial and operational flexibility to absorb delays or relocate programmes internationally.

Commercial clinical research should be recognised as strategic national infrastructure, not merely an optional activity. The objective is retention of clinical development which is a high value activity in itself as well as a critical part of the pathway to commercialisation. Delivery performance, speed and predictability should be explicitly measured, supported and rewarded. Guaranteed timelines, standardised contracts, coordinated site activation and clear escalation pathways could materially improve execution certainty. These reforms would benefit all sponsors while being particularly transformative for UK-headquartered SMEs.

Clearly there are current significant operational pressures within the NHS. Alignment of incentives in payment systems, supporting dedicated research capacity, and integration of research metrics into ICS performance frameworks could be considered.

Whilst domestic capacity remains constrained, pragmatism is warranted. It is important to be ambitious to increase phase I study activity in the UK, in order that temporary offshoring does not become permanent. However, phase I studies may sometimes be conducted internationally to access specialist infrastructure or accelerate initial clinical validation. In this case, UK policy should ensure that companies are able to return rapidly to the UK for subsequent development, retaining intellectual property, leadership and long-term economic activity domestically.

6. Public investment should be aligned more explicitly with long-term domestic economic return.

Where public capital materially supports early clinical development, mechanisms should exist to ensure that the UK participates in the upside created. This may include public equity or equity-like instruments via a national patient capital vehicle, revenue or milestone-based return tied to successful commercialisation that preserves investor incentives or IP-backed or royalty linked instruments where public money underwrites early risk. This could also be linked to incentives to locate manufacturing and high-skilled jobs in regions with existing clusters or higher deprivation.

Such mechanisms would align public investment with long-term national benefit, while reinforcing the sustainability of the funding system itself.

Thoughtful policy would be critical here to avoid crowding out private investors, avoiding government overreach in governance, and managing conflicts of interest when the state is both regulator/commissioner and the economic beneficiary.

These proposals represent intentionality.

None of these measures involve excluding international companies or undermining competition. Rather, they correct well-recognised market failures in a strategically important, capital-intensive sector. These must be underpinned by transparency, accountability, evaluation and public trust.

Eligibility should be based on transparent, objective criteria linked to economic activity, clinical development and national benefit, rather than company nationality alone. This ensures compliance with UK subsidy control principles and international trade obligations while still achieving the policy objective of strengthening domestic scale-up capacity.

Other leading Life Sciences nations already intervene deliberately at this stage of company development. The UK’s choice is not between neutrality and intervention, but between implicit intervention that enables value to migrate elsewhere and explicit intervention that ensures the UK captures a fair share of the economic return from its own scientific excellence.

If the UK’s Growth Mission is to succeed, scale-up must become an explicit policy objective, supported by coherent institutions, targeted funding and deliberate deployment of national capability.

References

UK Government (2023). Life Sciences Sector Plan.

Department for Science, Innovation and Technology.

https://www.gov.uk/government/publications/life-sciences-sector-plan

UK Government (2023). Commercial Clinical Trials Review (O’Shaughnessy Review).

Department of Health and Social Care.

https://www.gov.uk/government/publications/commercial-clinical-trials-review

UK Research and Innovation (2024). Explainer: UKRI Budget Allocations over the Spending Review Period.

https://www.ukri.org/publications/explainer-ukri-budget-allocations/

Office for Life Sciences (2023). Independent Review of the UK’s Translational Research Funding Landscape.

Delivered by the Centre for Process Innovation (CPI).

https://www.cpi.org.uk/our-work/projects/office-for-life-sciences/

Association of the British Pharmaceutical Industry (ABPI) (2024). Clinical Research in the UK: An Opportunity for Growth.

https://www.abpi.org.uk/medicine-discovery/clinical-research/

National Institute for Health and Care Research (NIHR) (2024). Research Delivery Network: Annual Performance and Participation Data.

https://www.nihr.ac.uk/explore-nihr/support/clinical-research-network.htm

Medicines and Healthcare products Regulatory Agency (MHRA) (2025). Clinical Trial Authorisation Application Statistics.

https://www.gov.uk/government/organisations/medicines-and-healthcare-products-regulatory-agency/about/statistics

European Commission (2024). Biotech and Biomanufacturing Initiative (Proposed EU Biotech Act).

https://commission.europa.eu/strategy-and-policy/priority-actions/biotech_en

National Institutes of Health (NIH). NIH Funding Mechanisms and Translational Research Programmes.

https://www.nih.gov/grants-funding

Advanced Research Projects Agency for Health (ARPA-H). Mission, Funding Model and Program Structure.

https://arpa-h.gov

Metsera, Inc. (2025). IPO and Acquisition Announcements and Investor Materials.

Public disclosures and regulatory filings.

https://investors.metsera.com